An economy with no shortage of story lines….

Few geopolitical developments in recent memory have so directly threatened global energy supply as the recently launched war between Iran and a U.S./Israeli coalition. At its center is the Strait of Hormuz – a 54-mile-long waterway through which roughly one in every five barrels of oil passes daily. Iranian forces have moved to take control over vessel transit, effectively dividing the Strait between an Iranian-controlled “tollbooth” corridor and a separately mined zone. At the time of this writing, the U.S. has responded to Iran’s so-called “tollbooth” by initiating its own blockade of the Strait. The Strait for now is almost completely closed to ship traffic. Regardless of whose warships or mines are responsible for the current disruption, oil is not flowing from the Persian Gulf, and global markets are severely suffering the consequences.

The economic ramifications of the massive supply disruption cannot be overstated. Economists estimate that even a prompt re-opening of the Strait could still shave approximately 0.4 percentage points from this year’s U.S. GDP growth and at least 0.3 percentage points from global GDP growth. The oil supply shock has driven crude oil prices sharply higher, and the recent economic data underscores the stakes. March CPI data has shown that the spike in U.S. gasoline prices has pushed headline inflation to its highest level in more than two years, breaking above the Federal Reserve’s upper-range target of 3.0%. The Pentagon also has requested $200 billion in supplemental funding related to the Iran engagement, an enormous figure given the Administration’s repeated assertions that U.S. involvement would be brief. America’s transformation into the world’s largest oil and gas producer provides meaningful economic insulation – an identical supply shock in the 1980s would have inflicted roughly twice the economic damage. However, insulation from the sharp increase in global energy prices is not immunity.

The human cost of the current situation is reflected starkly in the U.S.’s consumer confidence data. The University of Michigan’s Consumer Sentiment Survey has never recorded readings as negative as those registered in recent months with even self-identified Republicans reporting sentiment worse than at any point since the pandemic. Inflation expectations, while heavily partisan-influenced, have remained relatively stable with the first month of the conflict having had limited impact on either near- or longer-term forecasts. Whether the Strait remains blocked long enough to cause a broader inflationary spillover into non-energy prices remains the critical unanswered question.

Against this backdrop, the broader U.S. economy has demonstrated a degree of resilience though conditions fall well short of the robust expansion that current stock valuations seem to demand. Labor market reports have been frustratingly volatile recently with monthly payroll figures oscillating between modest contractions to outsized gains. Yet, corporate payrolls remain firm with the unemployment rate hovering at a near historic low of 4.3%.

On the trade front, tariffs – while no longer commanding daily headlines – remain an active legal and economic issue. In February, the Supreme Court ruled that the President lacked the authority to impose his recently enacted tariffs prompting the Administration to announce a new framework of tariffs, purportedly authorized by the Trade Act of 1974. Federal courts have since indicated that businesses subject to the prior tariffs may be entitled to refunds, adding yet another layer of uncertainty to the already deeply unsettled trade environment. On the fiscal front, early Congressional budget proposals for FY2027 point toward further spending increases and a widening deficit. We have raised alarm for a number of quarters that the nation’s fiscal trajectory is unsustainable; the current situation offer no reason to improve our assessment but rather to express yet greater concern. Given the enormous deficits, ~6.8% of GDP for the 2026 budget, which are being incurred during an economic expansion, we shudder to reflect upon the magnitude of deficits that will occur in the event of a U.S. recession.

Perhaps most concerning, and insufficiently appreciated by markets, is the continued erosion of the Federal Reserve’s independence. The Supreme Court blocked the Justice Department from subpoenaing Chair Powell on a trumped-up charge, yet this episode underscores the protracted campaign to subordinate the central bank to the White House’s authority. Meanwhile, the DOJ’s case to remove Fed Governor Lisa Cook remains pending with a ruling expected in July. Lastly, Senate confirmation of Fed Chair nominee Kevin Warsh remains at an impasse with key Banking Committee members withholding their support pending a complete withdrawal of the DOJ investigation of Chair Powell.

Compounding the stakes is the Administration’s overwhelming desire for lower mortgage rates so as to improve housing affordability. The White House is placing enormous political pressure on the incoming Fed Chair to ease interest rates prematurely. March mortgage applications fell by more than 10%, and meaningful relief for the housing market appears elusive so long as uncertainty around Fed policy and the Middle East conflict persists. We have previously expressed extreme concern about the catastrophic long-term consequences for inflation, interest rates, and the dollar’s reserve currency status in the event of a White House-controlled central bank. This risk has not diminished; if anything, recent events have brought this scenario meaningfully closer.

…as market volatility intensifies and valuations remain stretched

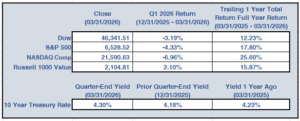

Volatility rose meaningfully in the first quarter of 2026 as equity markets endured a sharp decline in investor sentiment. Confidence in the AI-driven growth narrative has begun to crack with serious questions emerging around both the scale of future demand for AI infrastructure and the sustainability of the extraordinary capital outlays needed to support it. The S&P 500 declined 4%+ in the quarter, but the so-called “Magnificent Seven” mega-cap technology stocks fell roughly 11%, accounting for approximately 83% of the index’s total decline. The remaining index constituents cumulatively fell by just 1%. This concentration arithmetic cuts both ways — when a handful of names drive an index to record highs, they bear the heaviest burden on the way down. In sharp contrast, the Russell 100 value rallied by more than 2% for the quarter as the index has limited exposure to these seven tech firms. In general, since the conflict in the Middle East erupted, crude oil and equity prices have moved almost perfectly opposite to each other, underscoring how closely tied near-term market direction has become to the geopolitical arena.

Equity valuations, despite the quarter’s decline, remain historically elevated. The Shiller CAPE ratio continues to hover near levels last seen during the late-1990s dot-com era, and the forward price-to-earnings ratio sits well above its 30-year historical average. Corporate earnings have, to this point, provided a meaningful counterweight. Year-over-year EPS growth for the S&P 500 is expected to exceed 16% in 2026 as profit margins have reached their highest levels in more than two decades. That said, tariff-related cost pressures, a softening consumer confidence, and elevated financing costs all represent headwinds that have not yet been fully reflected in corporate results. This earnings season, and the forward guidance provided for the remainder of the year, will be particularly telling. Fixed income continues to reassert its value as a portfolio stabilizer with long-term Treasury yields approaching 5%, a level that compares favorably to equity earnings yields at current stock valuations.

What strikes us most is not any single risk in isolation — the Middle East conflict, the oil supply shock, tariff volatility, the U.S.’s fiscal trajectory, or threats to Fed independence — but rather the multitude of risks and their potential interactions. Markets appear to be largely looking past this group of risks, focusing instead on near-term earnings strength. This myopic posture can persist for longer than prudence might suggest, but it does not, in our view, justify complacency over current valuations. In this environment, maintaining disciplined diversification and sticking to a risk appropriate long-term investment strategy is not merely prudent — it is vital.

As always, we encourage you to reach out with any questions or concerns specific to your individual circumstances. The entire Dumaine team wishes you all a safe and enjoyable Spring season!